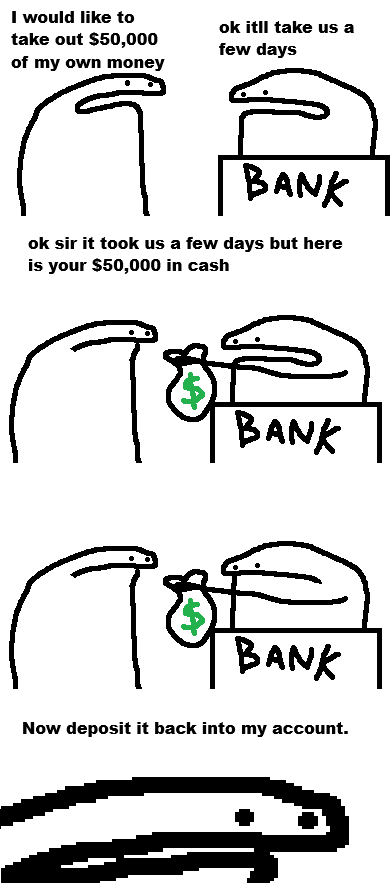

And next time have it when asked or we’ll do this again.

You can easily do a same-day wire transfer of this amount. Technically there’s no limit on the size of wire transfers. There’s probably a point where the bank will start asking questions, but car / mortgage down-payment sized transfers aren’t an issue.

But, yeah, I bet cash withdrawals are another ballgame. Not least because the bank probably doesn’t actually keep that much cash in typical customer-facing locations.

Is there not a security concern of doing basic checks before handing out cash?

For instance, elderly woman gets a text message telling her the IRS needs $50k cash or they’ll take her house. The bank says they need a few days, she complains that the IRS wants it now…and then they help explain that it’s likely a scam.

Yes, typically. I don’t know if that trumps “the bank has to give you your money when you ask for your money.”

And that is why it’s called a checking account. It’s only there for checking.

Of course, sir. Your 45 thousand will be deposited after we take the service fee

Lol imagine anyone having 50k

I have 50k in my hand right now.

It even has a cool picture of Ho Chi Minh on it

Uncle Ho always was a wily one.

Thank you for telling us about how much dong you’re holding.

You: buys a digital thing from an online store

Store: takes your money right away with no waiting time

You: Decide you don’t want it anymore, too expensive to renew

Store: okay, you’ll get your money back in 5 to 10 business days

I don’t think the store takes your money right away? They mark it paid when the transaction starts not when they receive the money.

Yes that’s correct, I’ve worked in the field, when you place an order online there’s a workflow triggered in the background between your bank, the vendor and visa/Mastercard in the case of credit cards. When you place the order, an authorization is placed on the card, at that stage it goes through a few checks (balance, fraud checks, creation of the transaction ID, etc). If it’s successful, it’ll move to a pending status, at this point it’s just an authorization, during this time the company will prepare your order for shipping. Once it ships, the authorisation gets converted to a settlement, which is when money actually starts getting transferred. Even then it’ll take a few more days for the banks to actually process the transaction before the vendor can refund it.

Of course, this is all just the way it’s done, I’m not saying it’s the right one. Companies use this process because it’s nice and safe, guarantees you won’t be losing money through the cracks, but nothing would stop them from just refunding before this whole transaction shenanigans is fine, they just take more risk.

Depends on the online store I guess, regardless, refunding the money always takes WAY longer

That is a bank rush. It’s how banks die if enough people do it.

In most countries it’s illegal to try get people to do one.

Hmm, are you still covered by the FDIC if you deliberately engineer a bank failure? Let’s say all of Bank of America’s customers decided that they just really wanted to fuck BoA hard. So they arrange to all demand the complete liquidations of their accounts, all at once. Or maybe people arrange a series of bank failures as part of some broader political movement. But hypothetically, if a group of people deliberately caused their bank to fail, would their deposits still be FDIC-insured? In other words, if you deliberately arrange a bank run, will you still be covered by FDIC insurance?

It exists to cover bank runs and it is your money. There is nothing wrong with wanting your money in any given moment. That’s just my take though, I’m not a lawyer.

I think it’d basically defeat its preventative purpose though if a story got out that people weren’t covered, even in an engineered bank run. What if you’re not in on the plot? What if it happens tomorrow at your bank? Are you just fucked too? Better withdraw all your money to be safe

What a potentially powerful tool of protest. Imagine if you got a movement of a few million people. They all move to a target bank. A few months later, they all demand their full account liquidation. Then you move on to the next megabank. One by one, drop them like flies.

With a few million people it doesn’t even need to be a specific bank. It would cause an enormous problem. Especially since we’re used to assets being digital these days. Request enough actual physical cash and it would rapidly reach a breaking point.

It’d be hard to prove a single participant. An organizer, maybe? But if you just heard everybody’s doing a bank run on the 20th and you’re scared of the stability of your bank, so you decide to withdraw your money on the 19th so you can put it into another bank, that seems reasonable.

(i know nothing about digital transfers between banks)

Hi, I don’t think my withdrawal of $20 from my collective accounts with BOA would really cause a failure… but I’m willing to try! Sincerely, -Poor

PS there are no ethical millionaires

I struggle to understand what modern insurance companies actually exist for, apart from money people donating money to them for nothing in return.

Insurance prevents people from hoarding money that they would need in case of a (personal) disaster to rebuild/repair/re-purchase their losses. If you know insurance will cover your house if it ever burns down, you spend the money, which helps the economy.

Huh? Most people don’t have enough cash to pay off their home, let alone save up enough to be able to buy a backup home. That’s what insurance is for- it protects you from expenses that would be ruinous if you had to pay them out of pocket. The insurance company takes in more than it pays out, but it’s worth it for home insurance (and health insurance in the good old US of A). It’s why buying insurance on some $100 tech thing is always a ripoff.

Even if someone worked very diligently to save money, it would take a whole lot to save enough to be able to afford an entire second house.

Some are mandated, like auto insurance. Some are because your relative loss from buying insurance is waaaaaaaay less than your loss from an actual disaster. I for one don’t mind paying (and this is an example, lol, like I can afford a home in my area) $200k over 40 years when the cost to rebuild my home after a fire, flood, hurricane, tornado, earthquake, or godzilla would be >$400k.

Health insurance is the real head scratcher. It’s almost a guarantee that you’ll need it at some point. Pet insurance falls under this as well. A friend was telling me that it was a no brainer unless you’re the type to shoot the dog as soon as it gets mildly sick. It’s something along the lines of $40 a month, which means you’re paying $480 a year, or maybe $4,800-$9,600 over the 10-20 year lifespan of the dog (it’s a dog in this example because my fingers like the d more than the c). You know how much a single emergency with a dog can cost? Probably the entire amount you’d pay over a 10 year life span. If it is a longer problem, it balloons even more. And, importantly, right now pet insurance is where health insurance was at years ago, where they didn’t scratch out your eyeballs over every payment. It may take that turn here soon, once the industry is more established. That’s what my buddy actually wants to do, is review cases for pet insurance companies. I might have to toss him out of the car one day if it gets to the point of our human health insurance.

I might have to toss him out of the car one day if it gets to the point of our human health insurance.

Just take him for a walk…

His spouse might have a problem with that, or I’d already have the leash ready.

(it’s a dog in this example because my fingers like the d more than the c)

Come again?

This stopped me in my tracks also lmao. I was wondering how you get vet bills from playing red rocket.

See, if I liked the c more than the d, I would be using a cat as an example. You know… typing? My fingers like the d, which is on the home keys, more than the c, which is a downwards reach.

This isn’t one you can dig yourself out of.

Yeah, let’s throw this poor person a bone already so that they do not have to dig their buried one up.

deleted by creator

It is reverse gambling.

Except when you need the insurance it is gambling whether you get it.

Funny that this came up in my feed immediately after: https://www.bitsaboutmoney.com/archive/two-americas-one-bank-branch/

Infinite money glitch.

{kind=link}