I don’t think there is an earlier option for less money anymore but could be wrong.

At this point I’m just assuming that by the time I’m “retirement age” there won’t be any social security anymore, and I’ll just have to keep working until the day I either drop dead or win the lottery

Even if social security was still paying out it’s not like you could retire on it anyway. You need a lot more.

Start an IRA and put a few bucks a month in to buy shares of a mutual fund. Every penny you can invest in retirement will pay off when you do retire, and the sooner you can start, the better.

No average year of IRA return will beat the 6.8% interest or more that a lot of us are paying on student loans debt.

Literally the old people stealing the wealth of future generations

Before that you had to work until you died or couldn’t physically do it any more and starved.

Grateful we aren’t at that point again, yet.

Over the lifetime of the investment account, it should outperform the interest you’re paying. You don’t want to track your retirement investments from year to year since the market constantly fluctuates, but it’ll still trend up 6-9%.

I’ll certainly drop before I am able to retire.

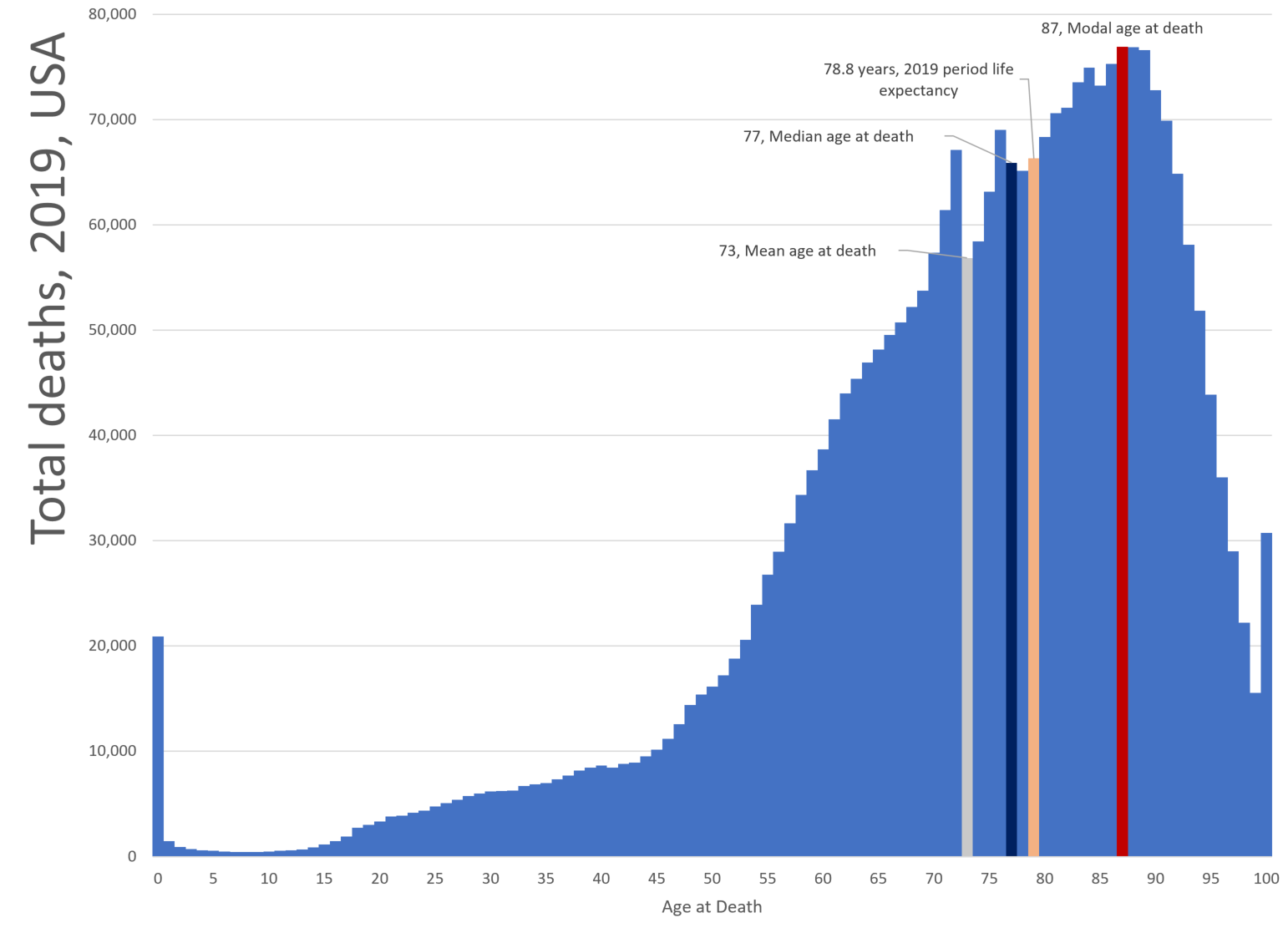

men’s life expectancy is only 77 now

That figure is average life expectancy. IE 50% of US man are expected to reach 77.

A bit of history on why 65 was originally set as the retirement age.

The first country to set retirement at 65 was the Weimar Republic in Germany (1918-1933).

The reason 65 was chosen was that at that time only 5% (1 in 20) of the German population made it to 65. Retirement and the pension was a case of “You have worked hard all you life and will die soon, this is to let your final years be a bit easy”

Over the last century, in the west at least, over average lifespan has increased markedly and the quality of life for people of advanced age has also increased.

Many government now face the issue that they cannot afford to keep paying retirement benefits for two reasons:

1: Many many more people are reaching retirement age and they are living for decades more, rather than a few years.

2: With the decline in birthrates the ratio of working people to those in retirement has changed from about 10 to 1 to about 5 to 1 and is expected to get worse in the decades to come.

This does not answer your question but gives you an idea of the issues and hard decisions societies will have to face in the coming decades.

deleted by creator

In the US, social security is a tax on poor people earning less than~$160k. That’s the bottom 90% of earners.

The top 10% of earners collect about half of the country’s personal income. Each of them does have to pay SS tax on the first $160k of earned income, but clearly there’s a huge pool of income that doesn’t pay into social security.

To that point SS is fully funded till about 2035 and then can pay out approx 75% of benefits after that. Removing that $160K cap would pretty much solve things.

But the rich don’t want to pay poor people’s retirement, that’s for the poor people to handle

deleted by creator

That figure is average life expectancy. IE 50% of US man are expected to reach 77.

I can’t access the full paper that this is in reference too, so I’m not sure how they calculate it… but isn’t life expectancy usually the mean age of death? I would expect the distribution to have a left skew from people who die young, which should mean that more than 50% of US men are expected to reach 77.

average life expectancy

mean age of death?

To me mean = average, so the two statements are the same.

Are you talking about median age of death?

When child mortality was very high (pre- 20 century) that was definitely the case. I am not so sure that it is now. I feel that average life expectancy will be a lot closer to 50% survival rate (median age of death) than it was in the past.

To me mean = average, so the two statements are the same.

Are you talking about median age of death?

The median is the midpoint of a sample, not the mean. So, the median point represents the age where 50% of people will live to, the mean does not represent that (it’s often relatively close to the median assuming the data doesn’t have too much skew, but it can be way off).

When child mortality was very high (pre- 20 century) that was definitely the case. I am not so sure that it is now. I feel that average life expectancy will be a lot closer to 50% survival rate (median age of death) than it was in the past.

There are still plenty of people who die young, even though child mortality is less of a factor in wealthy countries right now. Plenty of people die in car accidents at a relatively young age, for instance. I’m sure the median and mean aren’t like 10 years off of each other, but I wouldn’t be surprised if they’re 3 or even 5 years off, which could be pretty significant in this context.

Well, both of us are making assumptions without doing the research.

So. I respect your opinion but neither of us knows that we are actually correct.

Well, the definition of the mean and median of a sample doesn’t depend on the particular data set, and there’s plenty of non-age related causes of death in the world which would logically skew the distribution to the left! You can look at actuarial tables to see this in action:

https://www.ssa.gov/oact/STATS/table4c6.html

Male life expectancy at birth in this table is 74.12, but you’ll notice that you don’t get to 50% of the population dying until somewhere between the ages of 78 and 79.

This website has a pretty good chart showing the skew for a 2019 dataset:

Where are you getting the 70 years old number combined with the “have to wait until” logic?

In the USA you can start taking Social Security at as young as 62, with most waiting until 67 for full benefits. The only folks waiting until 70 are those that want even MORE than the full benefit.

I think they’re assuming retirement age will be raised by the time they retire.

If the pattern follows from the last age raise (from 65 to 67) then the people that will be affected by an “age 70 for full benefits” may not even be born yet. The last age raise started in 1983 and just came into full effect in 2022 (for only a 2 year age increase).

Social security will be bankrupt by 2033 according to their own estimates.

https://www.ssa.gov/OACT/TRSUM/index.html

Somehow they expect to pay 80% benefits beyond that point.

Expect your income taxes to go up…and by a lot.

They don’t expect to go bankrupt by 2033. That’s when the surplus/reserves will run out. The system doesn’t have the fixed amount of money. Current employees are constantly paying into it.

20% is the shortfall between payout vs people paying in. And it will only happen if it’s not addressed. Which I’m sure will get addressed last minute or something like that.

You can start collecting at 62 and get 70% of your computed payout, which I will be doing.

The math is too hard for me given inflation and all that, but since social security rarely seems to have enough money, I’d guess they’re still paying out more than they take in…?

If you make it to 62, your life expectancy is 21 more years. that mean 21*0.7 = 14.7 years worth of social security payments. Full benefit at age 67 gets you 16 years worth of payments. If they’d raise full retirement age to 70, you’d only collect 13 years of payments.

I’ve been coached into waiting until age 70 to get 100% of the payout. If you cash in at age 62, even once you hit 70 you’ll still be getting 70% of your payout. Could you bear to wait eight more years for the 100%? You’ve already waited 62 years! What’s 8 more?

8 years is a long time and cancer can kill you in two, especially if you don’t have good doctors and they don’t catch that it metastasized already. Ask me how I know.

8 years are 2 election cycles. Much can happen in that time.

Could you bear to wait eight more years for the 100%? You’ve already waited 62 years! What’s 8 more?

It’s easy to think that way in your younger years. That’s a much more difficult request for people actually in their 60’s, lots of people make it to that age with broken down bodies, various illnesses/prescriptions/whatnot & probably can’t see themselves continuing to do the work thing throughout their 60’s let alone 70.

There’s also the problem of holding down a job at that age, ageism exists in a lot of industries so a lot of these people are first in line for layoffs / taking a massive pay cut from their earlier jobs vs being a Walmart greeter or just being unemployed.

But sure… in theory if you manage to stay fit & healthy well into your old age & are able to hold onto your normal job then sure working into your 70’s or more could be plausible. People probably worry less about that stuff once they’re higher up on the corporate ladder - though at that point they should already have fat 401K plans & other investments so the social security aspect becomes less relevant.

Just wanted to chime in and say that everyone should start investing in their retirement as early as possible. Even if it’s just a few bucks a month, it’ll make a big difference down the road.

My dad waited until 70, and then by age 72 began a severe decline in health which eventually saw him homebound with a feeding tube, only leaving the house for doc appts or trips to the ER. I am quite certain if he had a do-over he would have retired earlier and enjoyed his 60s instead of working at his boring job.

I think if you reach 62 and you’re gainfully employed and truly enjoy what you do, there’s nothing wrong with holding out for more benefits. But if you are able to retire earlier, I can’t recommend continuing to spend your days doing work you don’t enjoy because “what’s 8 more years”. Those 8 years could be your big chance to enjoy the fruits of your labor.

But what if you invest it for those 8 years?

Removed by mod

deleted by creator

There is an early option for less money.

You can start at 62 but you get twice as much if you wait until 70.

What a gamble.

What’s twice as much as $0?

I get $2,177 a month at 62, $2,681 at 65 (Medicare age), and $3,836 at 70. I also have a pension, and a 401K. There is an incentive to work longer, but I don’t need to. Most of the people I work with retire around 65.

Don’t watch kurzgesagt’s video on “South Korea”* getting older, if you don’t want to know the awful answer to that.

People will have and get social security paid. But the environment wars and mass immigration will be the answer, which means you’ll be looking at 20 years of conservatives bitching and whining.

Want to avoid it on a personal level? Emigrate to north europe. Sad, but it is what it is.

* video is more general than that. But they used korea as the clickbait.

I don’t think there is an earlier option for less money

Sure there is, go to the SSA website itself the earliest eligibility is 62

https://www.ssa.gov/retirement/eligibility

You can also register yourself there & see your own estimates based on when you expect to claim social security.

You really need a Vegas odds maker and and epigenetics expert to figure the over and under.

I’m 62 I’m hoping to work to 65-70 to get as much as I can before I kick the bucket.

Uh no, if they did then everyone that lived past average life expectancy would have issues.

I expect the issue will need to get addressed in the future, especially as the wave of millennials retiring will be far worse than the boomer wave.

I wouldn’t be surprised if it gets combined with a change in qualification age for Medicare. You push Social Security age qualifications up but push Medicare down to put the added healthcare costs on the Federal Government instead of the states. It would likely involve a slow ratchet up rather than an immediate jump. I can also see the deal include ditching the social security tax cap, or maybe adding a new tier.

Social security never made any sense to me anyway. Why not just make the economy healthy so that people can save into old age? Perhaps invest a little into financial literacy so someone doesn’t blow all their savings in Vegas when they’re 45. It’s frustrating the the government’s like, “You can’t spend that money. We don’t think you’re smart enough to plan for the future, but we’re ethical enough we’ll keep it for you and return it to you when you’re old and grouchy.”

The federal government is the sole issuer of currency. When the federal government spends, it credits recipients accounts with the press of a keystroke. The money is created from nowhere. When the federal government collects taxes (social security, etc) it debits the accounts of taxpayers effectively deleting that money from existence. If the government issued social security payments that exceeded the amount it collected, it would be creating money, which is one of its functions.

This is not at all how the federal reserve and treasury department work.

The fed does create money, but not directly. They control the reserve rate, which determines how much banks can lend over backed deposits, which in turn affects the amount of currency (not just physical but also digital) in circulation.

They can also issue or absord treasury notes and bonds to impact money supply, though this is fairly small compared to the first method.

Lastly, the treasury can print physical, paper or coinage money. This called “fiat currency” by the way. This, however, accounts for an even smaller portion of the moneg supply than bonds.

In short, the government cannot, does not, and will not simply “create money from nowhere.”

Please avoid posting false information.

Federal Reserve Bank Chairman Ben Bernanke says that money is spent by the federal government simply by changing numbers in bank accounts.

"For further support we can just listen to Federal Reserve Bank Chairman Ben Bernanke. When asked “Is that tax money that the Fed is spending?” he replied, “ It’s not tax money. The banks have accounts with the Fed, much the same way that you have an account in a commercial bank. So, to lend to a bank, we simply use the computer to mark up the size of the account that they have with the Fed.” Mosler says, “the Chairman of the Federal Reserve Bank is telling us in plain English that they give out money (spend and lend) simply by changing numbers in bank accounts. There is no such thing as having to ‘get’ taxes (or borrow) to make a spreadsheet entry that we call ‘government spending’.”

It is that simple. How does the government spend? “Keystrokes,” says Wray. The money does not come from anywhere, it is created by the currency-issuer. Thus, taxing and spending are functionally two completely separate operations. The government issues the money with a few keystrokes at the Fed first, and then it taxes, removing some from circulation."

https://medium.com/@nicholasadiaz7/on-the-role-of-taxes-mmt-707fb4b3b80b

When the government approves civil projects such as infrastructure projects, the payments are considered issuing of currency according to modern monetary theory.

From Wikipedia regarding governments with Fiat currency: “When a government spends money, its treasury credits its operating account at its central bank and deposits this money into private bank accounts. This money increases the total deposits in the commercial bank sector.”